On April 6 we submitted an application to the bank's portal, which included the standard federal form with information like average payroll and headcount.

On April 8 we received an email saying that we needed to submit some additional information, which just turned out to be repetition of payroll information we had already listed on the federal form.

On April 13 we received another email asking us to submit ownership details for any equity holders in our LLC.

It's now April 17 and we have not heard anything back. If I call the bank's number, I get a recording which says they'll process our application as soon as possible and they're unable to provide status updates over the phone.

Now I'm reading reports that the program is already out of money. If this is what's supposed to help small- and medium-sized businesses weather the pandemic, it is not inspiring much confidence. Have others had a similar experience?

Second off, we're already tooling up for the second round of SBA to get more loans through the system by eliminating a lot of manual processing. So have some hope and contact your reps and senators - we're already getting ready to get loans through once they open up the program again.

1) The SBA was approving PPP submissions in like an hour (rubberstamping).

2) Any delay was 100% your bank. Many banks just didnt get to applications but didnt notify people. Some banks said people were approved (by the bank) but didnt submit those people to the SBA

3) There was a lot of time to submit to intermediaries like paypal. Paypal was turning applications around in 24 hours to funding. There were people that applied on 4/3 with a big bank that didnt get it and people that applied thursday night through paypal that got it

4) Big banks often added additional criteria which made it harder to complete the application. Some big banks were not using the correct calculations

5) Once you have an SBA loan number you are good and money is allocated. Banks have 10 days to disburse the funds

6) The SBA ran out of allocated funds, not all the money has been disbursed.

7) People submitted to multiple lenders and it was fine

Overall I think the program went pretty well and there was plenty of time for people to get applications in. There was obviously working of the system (hedge funds, large restaurant chains, etc) but if you look at the distribution of funds there were still many many small loans.

750K under $150K with an average of $51K

I spent the last 2 weeks doing nothing but reading reports, stats etc about the program to ensure I was able to get it for my team. Lots of people submitted with a big bank and just waited accepting no updates, now are complaining after it is over.

SVB:

- SVB loses a big check of ours for a week prior to PPP

- SVB takes 1 week to get their newly developed PPP portal active

- SVB prioritizes new clients and bigger accounts (allegedly, see Twitter screenshots)

- Delays and bugs once it's live

- Local bank tracks and finds lost check, makes except to deposit

- Local bank puts out a low-tech, but reliable DocuSign PPP form the day after announcement (and 6 days before SVB's portal taking PPP apps)

- Local bank prioritizes existing clients

- No bugs, you can connect with them in <10 mins to talk to a repApplied on the first day they opened their portal, which was a few days after the program started.

Got an error on the second page of the app when I told them I am C Corp, was told the portal wasn't ready for C Corps yet.

Got an email the next day to try again, and did so and it worked.

Got a promissory note automatically at the end of the application which just needed a few bits of info and my payroll worksheet from Gusto.

Was informed this morning that the program was out of money and they would let me know if/when the program had more money to fund the loan.

Oh and through the entire process Chase has stressed that my local banker has no information, no access to the system, and no way to help me, so not even bother trying to talk to them.

Both have existing checking + lending relationship with BoA.

Company #1 is 5 years old, Company #2 is 6 months old.

4/3: Both companies applied

4/6: Both companies submitted all required docs

4/8: Received a call about Company #2 - claimed we could only use 2019 payroll to determine size of loan. Incorrect - new co's can use Jan/Feb. Told the rep this. Was told I would received a callback.

4/9: Received a promissory note for Company #1, signed and submitted.

4/10-4/15: Received numerous automated calls + emails asking me to do things I already had done.

4/16: Received a request to update business info for Company #1. Did so. Rep said I should expect deposit of funds in 1-5 days.

Still nothing on Company #2. I am tentative that the $$$ is allocated already as we have been assigned an SBA loan number.

BoA did some things right (opened up first), some things arguably right (as someone who has a previous relationship, I appreciate getting prioritized), and some things terribly (having people take time to give reminders on actions that have already been taken, having no one available to answer questions or provide support, etc.)

People are sharpening their pitchfork tines...

* Wave Life Sciences, a biotech company incorporated in Singapore, got $7.2 million for the 97% of the company’s work force based in the United States. https://www.sec.gov/Archives/edgar/data/1631574/000119312520...

* Potbelly Sandwich Shop, a chain of 400 restaurants, got $10 million for its 6,000 employees. https://www.sec.gov/Archives/edgar/data/1195734/000119312520...

* Texas Taco Cabana, a chain of 121 Mexican food restaurants, got $10 million https://www.sec.gov/Archives/edgar/data/1534992/000153499220...

* Ruth’s Hospitality Group, a Florida-based steakhouse operator, got $20 million for its 5,700 employees. https://www.sec.gov/Archives/edgar/data/1324272/000156459020...

When we first heard whispers about the program, we reached out to our banker who responded that they had heard the same whispers but didn't have anything concrete to tell us. The bank suggested that we start gathering financial paperwork (as government contractors we tend to need those statements to respond to audits, so this was easy for us.)

During the first week of April, our bank sent us the preliminary application form, told us to look it over and make sure we have everything we need. A week later the program officially opened, but since SBA hadn't offered specific guidance, the bank wasn't accepting applications yet.

On the morning of April 6, our bank opened the "official" portal to take applications. We immediately jumped into it, only to find the portal had a couple of show-stopping bugs and some of the instructions were ambiguous. Our frazzled representative told us that the bugs were being worked on and to keep trying. We did, and we were able so successfully submit out application later that afternoon.

While on a walk on Easter Sunday, we got an unofficial email from our banker that the application had been approved, which was followed up by a more official email yesterday. No word yet on when the money will actually hit our bank account.

I presume that our relationship with our bank helped things go smoothly. While we weren't 100% sure that we submitted the right documents for everything, the bank has most of our financial info through other dealings so they may have been able to check all the right boxes.

So we applied with 6 different banks, all small around the country. that didn't work.

Found and applied to a very small bank in rural MN (where we are) and got a person on the phone finally. Submitted to SBA after 7 days, and then got a SBA loan number and approval on 4/14 (just before it ran out).

Now they said I won't be able to close on the loan and get the money until 4/24.

I don't even know what the takeaway is at this point.

My advice is: continue to work with your lender to get your application squared away so that it's fully ready to be submitted to the SBA as soon as additional funds are allocated (since I can't imagine that those will last long either.)

(In the interest of full disclosure, I'm Pilot's CEO. We don't do anything with PPP loans directly but it's an area of significant interest to our customer base, so we've been following it closely and have been pretty regularly releasing updates like this one from yesterday: https://pilot.com/blog/the-ppp-has-run-out-of-money-now-what...)

We had everything prepared thanks to Gusto and submitted. But it may not matter because they had us wait to the point of it no longer being available. We’re laying people off starting Monday. :/

I went through a similar process with Bank of America. I submitted my application on Friday when it opened. Then documents. A few days later, I got a call from a Bank of America representative. He asked if I had any issues. The rep tried to verify our business information. I spent some time trying to verify that he's not a scammer. I'm from Washington. He's in Colorado. He told me he's a mortgage banker. :) He's polite, but he has no idea about my application status. He just got assigned to reach out. I told him I uploaded the docs after lots of confusion. But I think I got it. The rep told me that I can't call him for information on the application. :)

On April 15, I received an email asking for business information. The email said, login, click "I'm ready" and fill out the required information. I tried to verify that it's a legit email. I avoid clicking on the link. :) I have no idea what the required information is. I logged into my business account, but not prompted "I'm ready" button. I spent 30 minutes looking around for the button. :) I found that I need to update my account information and promptly did.

On April 16, I saw the news that PPP is out of money. I'm worried. I log in to my business account again. This time, I got prompted the "I'm ready" button. I filled out the required information about our business.

I haven't seen anything after that.

There're a lot of people that I can get mad at, the virus, the rep, the bank, the state, the government, China. At this point, I don't think those things matter. Stay safe.

In a similar vein, my university recently received 38 million dollars through the cares act, half of which is required to be distributed directly to students. The administration has not said a word about that money, but has confirmed we still need to pay fees for services that we cannot use anymore, like the shuttles or the gym.

I never really thought about corruption in the United States before this.

If you have an application in process, keep it going. If your bank is still taking applications, file one.

Most members of Congress agree that the CARES Act small business programs should get more funding. But they are dragging their feet on a bill because of other topics and ideas that could get attached to it.

The more un-fulfilled applications there are waiting for funds, the more heat that banks and trade associations can put on Congress to move fast. It demonstrates the dire need.

And if more funds are allocated, banks will likely start disbursing them first to applications that are already in the queue.

You should absolutely be contacting your House representative and Senators about this. Call their office, tweet @ them, send them emails. Tell them to pass a bill on Monday to fix this.

https://www.house.gov/representatives/find-your-representati...

https://www.senate.gov/general/contact_information/senators_...

It's rumored that, just like how BofA prioritized companies with active business loans, other banks are giving money to ensure their loan customers can continue to pay existing loans.

We have almost 40 employees and bank with Chase and Wells but we realized early on that the big money-center banks were a couple of steps behind are were going to be overwhelmed.

We started by looking at the full list of PPP banks and identifying the most tech-savvy of the bunch https://heavy.com/news/2020/04/apply-payroll-protection-prog...

Eventually after applying with a few we got furthest with by applying via Kabbage and SmartBizLoans. Our company had an existing relationship w/these lenders and they seem to be the most tech-conscious of the bunch.

Our application via SmartBizLoans was approved on 4/13 and the funds deposited on 4/15. SmartBizLoans acts as a broker to a number of smaller banks which might explain why they were quicker. AMA, glad to help.

Didn't hear anything else after that.

For my company we went through Chase the same day when it was available. They never asked for any information. We called, they said it was being processed. Still no info.

I have a few other friends who own businesses and none have received the loan. The only person I know that received the loan went through a local bank in New Mexico. I think the big banks just prioritized the really large loans > $1M.

Our bank said they were still doing diligence on all applications upfront before submitting the loans to the SBA even though the bank isn't actually liable for anything. This was causing about a 2 day lag time from starting to process the loan application to submitting it to the SBA. In our case that meant not getting the loan submitted before the funding ran out.

Let's just say this thing is one of the biggest scandal in the history of modern USA. Clearly some banks did favour some "small businesses" over others by restricting application dates.

Haven't heard anything, not expecting anything, it's pretty discouraging...

She submitted on the first day that US Bank allowed applications. She then spent the next 4 days going back and Forth with US Bank over her paperwork. She had a loan approval from US Bank, and then...nothing.

...until Wednesday, when she got an email saying that the funding had ran out.

My mom plans on keeping her staff employed while they work from home for as long as she can, but, she had enough money to run payroll on the 15th, and will probably not have enough money to run payroll at the end of the month -- hospitals have stopped having elective surgeries, and many of them are 60+ days behind on their bills right now.

I know that the banks were hammered with applications and there are a lot of people who are in the same situation as her. I'm hoping that when they add funding to the program, that businesses like hers (who were approved provisionally, but ran out of money) would be processed first.

Applied with a big bank, get nothing.

Applied with a small bank, got lucky if you applied early on April 3rd

?

Edit: we applied with a small bank at 6am on the 3rd and got funds earlier this week.

https://www.sba.gov/sites/default/files/2020-04/PPP%20Deck%2...

Sure enough, the local bank (Quantum National Bank) in GA, got back to me with an application to fill out before Chase even had a "form" to register interest in the program. They had a plan, and their banker was responsive via phone and email. It was pleasantly not a bad process at all.

We signed our closing papers today.

I stupidly dragged my feet in re-submitting, given all the steps required. Finally got it re-submitted yesterday, just as they announced the well's run dry.

PNC kindly got back to me today (via phone) and had me add one more piece of missing info, in readiness for the next wave of funding (if that happens).

Now I wonder if I had responded immediately last week if it might have made it under the wire. I guess who knows?

And why on earth do you still use cheques?

The highlights of the report:

* 1.6 million loans worth $342 billion approved through 4,975 lenders

* California, Texas and New York accounted for 23% of the loans, more than $82 billion. (see Reuters graphic: https://fingfx.thomsonreuters.com/gfx/editorcharts/qmypmrzyv...)

* Number of loans approved per 1,000 small businesses was the highest for rural states (see Reuters graphic: https://fingfx.thomsonreuters.com/gfx/editorcharts/xlbpgxaov...)

* A breakdown of loans per industry shows that construction and manufacturing firms were awarded loan amounts disproportionately higher than the share of employees in that sector. (See Reuters graphic: https://fingfx.thomsonreuters.com/gfx/editorcharts/qzjvqlbop...)

* The top lender processed $14 billion in loans across 27,307 businesses, with $515,304 average loan amount.

* The lender with the most number of loans processed $2.9 billion to 40,746 businesses with $72,803 average loan amount.

More analysis here: https://www.reuters.com/article/us-health-coronavirus-usa-le...

My local credit union is not SBA. I applied through a few online brokers; got word a few days ago my application was approved and sent to the underwriter. Later that day it was announced all the funding was dry.

Never any updates, not even a confirmation email.

Checking the status today, looks like they never got through processing and submitting to SBA. So looks like we missed the boat.

It’s very likely that the allocated funds actually ran out within 1-2 days of applications.

The allocated funds were so paltry that whether you got it or not was based on luck. If you happened to pick a good bank with a short queue or good processing, or if your own bank prioritized you, then you were in luck. In my case our application didn’t even get reviewed the whole time, and the applying only one time rule blocked us from seeking some better bank.

Where can I buy a case?

We're a software firm that does contract work for airlines, so that may have also helped out?

The general sentiment in this thread seems to be that large banks absolutely suck for a bunch of reasons.

What would happen if I apply for the same loan through some other smaller local bank or credit union? As long as I only accept the loan through one place, it should be fine, right?

We were able to get the loan amount in our account earlier this week.

We're ~30 employees (~$7M annual revenue) located in the Midwest. I wasn't directly involved with the application, however.

Sorry to hear of the troubles you're going through, these are not easy times.

I'm amazed it went as well as it did. Government bureaucracy isn't designed to try new things or deal with bumps in the road as they appear.

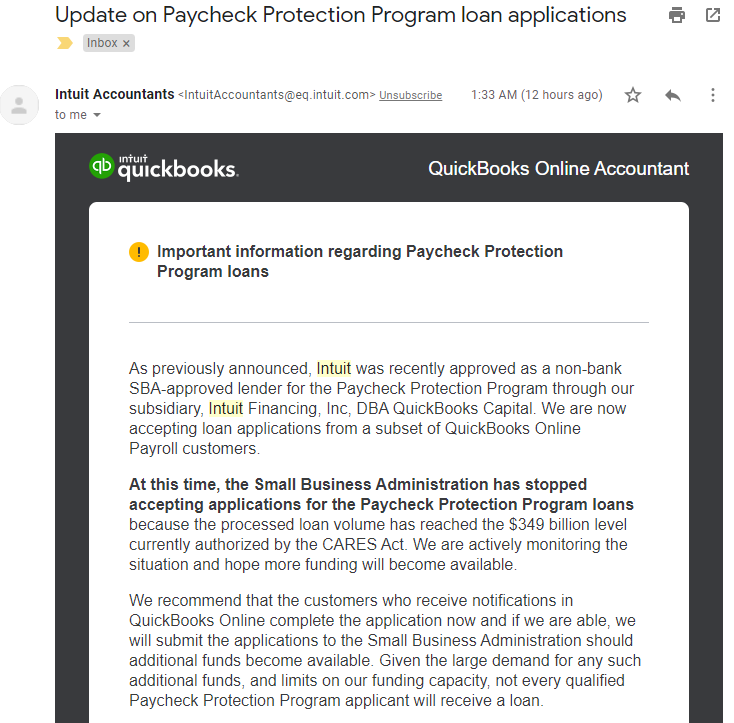

Correct, I received an email from Intuit today stating that the loan volume has been hit: https://i.judge.sh/ashamed/Derpy/chrome_YyblB6Znpm.png

1) If the SBA received your application then you should see a inquiry on your credit report. CreditKarma is a good free choice to check your report.

2) Chase and other big banks added additional language to their loan contracts that allows them to sue for defaults. Read the terms carefully before signing.

What are the downsides, theoretical or otherwise, of taking this money?

It’s all very frustrating.

{kind=link}